Buy Now, Pay Later (BNPL) is a term that describes short-term financing of items, typically with no interest (at least if you make your payments on time). In today’s culture, there is a huge rise in consumer debt, as people are given the ability to buy things they cannot afford. In 2022, credit card companies charged borrowers over $105 billion in interest and $25 billion in fees. Data from 2022 also revealed that those who did not make payments on time and had a revolving balance paid more interest and fees than they earned in rewards. One 2023 study found that, at the time, 89 percent of Americans with revolving credit card debt were trying to pay it off within the next year, but 50 percent reported feeling as though they might not because of the rising costs of goods. Instead of saving money and buying everyday consumer items with cash, many are buying items on credit. It is one thing to finance larger purchases, but when someone buys a $200 pair of shoes by making four $50 payments, we might have a problem at hand.

The requirements for using BNPL are very low. Typically, there is no minimum credit score, and all you need is a cell phone number and proof that you are over the age of eighteen. In 2024, fifteen percent of Americans used BNPL—an increase from 14 percent in 2023, and 12 percent in 2022. Additionally, 24 percent of Americans who have used BNPL have made a late payment, and nearly 40 percent of Americans regret using BNPL when they realize the total costs. Further, a study from last year that observed the spending patterns of 275,000 consumers at a major American online retailer reported that people were 9 percent more likely to make purchases when choosing a BNPL option, and those who used BNPL spent more money and left the website with purchases totaling 10 percent more, on average. These statistics clearly show that consumers are experiencing negative consequences from their use of BNPL.

The Things Unseen

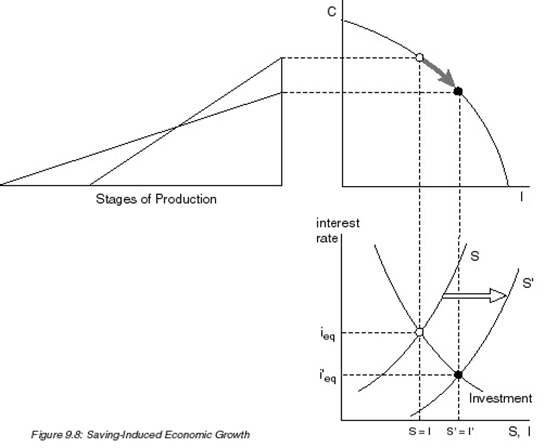

Would such a state of affairs exist in a society with sound money and interest rates based on consumers’ time preference? Roger Garrison’s Austrian business cycle theory framework shows a wedge that develops between saving and investment in the loanable funds market when there is an artificial credit expansion. The lower interest rate due to the credit expansion leads individuals to save even less than they otherwise would.

The low interest rates not only discourage saving but encourage even greater consumption financed by cheap credit. What is unseen is the savings that people otherwise would engage in, along with all the concomitant low time preference behaviors associated with it, such as family formation and planning for future generations, as well as the avoidance of crippling debt.

A Psychological Problem

Buy Now, Pay Later could objectively work (if financed by real saving), but the human desire to get things now creates a problem that often leads to being trapped in consumer debt. Ideally, if one is buying a low-value item, the individual would pay for the item in cash. Moreover, if the individual does not have cash to pay for the item, he or she would not get the item. For those who would not choose to go into debt, the very fact that fiat credits are an option incites them to go into debt.

Furthermore, when one can gain access to a good that he does not have the money to buy—without incurring fees or interest—it is appealing. The appeal to immediate gratification leads the person to buy goods that he cannot afford. Recent survey results have revealed that, for many Americans, BNPL purchases are not just for luxuries, rather, 33 percent of individuals use BNPL to bridge the gap between their paychecks, which is up from 30 percent a year ago and 27 percent the year before. Furthermore, the survey reports that nearly half (49 percent) of BNPL users say that BNPL is their choice of payment for “stretch” purchases. Our society has created an atmosphere that encourages living beyond one’s means; the fantasy has been created by a kind of magical thinking that promotes luxury consumption as self-care.

Conclusion

Human nature desires immediate gratification, and the desire for immediate gratification—along with the other cultural effects of inflation—is what has led to the idea of BNPL becoming normal. Although it seems harmless, as previously evidenced, BNPL schemes often lead to debt because of added fees or interest that come when the person does not pay on time. As the Federal Reserve has made it easier for many, including young individuals, to gain access to credit, our society has become caught in a cycle of debt-fueled consumption that we do not have the money for. Additionally, the inflation created by the Federal Reserve continues to discourage young individuals from saving and planning for the long-term. The discouragement from saving includes the fact that big purchases that are life milestones, such as buying a house, seem unattainable, and people do not see the point in saving. As Mises noted,

…inflation…shakes the foundations of a country’s social structure. The millions who see themselves deprived of security and well-being become desperate. The realization that they have lost all or most all of what they had set aside for a rainy day radicalizes their entire outlook…. The effect of such an experience is especially strong among the youth. They learn to live in the present and scorn those who try to teach them “old-fashioned” morality and thrift.

Although individuals believe they are benefiting from BNPL, it is likely that BNPL schemes will continuously lead individuals to buy things they do not have the money for, putting them in an unstable financial position. When you give individuals access to something at the instant they desire to have it, it is not often that they turn it down. The immediate gratification obtained through BNPL opportunities might seem good at first, but when it causes individuals to become entrapped in debt and discourages them from saving, it leads to poor financial health and societal decay.